May 2026 Market Update: Record Highs, Rising Rates, Inflation, and a New Fed Chair

- Summit Puri

- Jun 2

- 4 min read

May proved to be a notable month for investors, with major U.S. equity indices climbing to new all-time highs even as the bond market contended with persistent inflation concerns. The S&P 500 crossed 7,500 for the first time, buoyed by resilient technology sector performance. Long-term interest rates surged to near two-decade highs before retreating as oil prices eased. Hopes surrounding a potential peace deal in Iran also provided some support to markets, though the situation continues to evolve.

The month also marked the first leadership change at the Federal Reserve since 2018, with Kevin Warsh sworn in as the new Fed Chair. Although transitions at the Fed can raise questions about monetary policy, history demonstrates that markets and the broader economy have fared well under a variety of Fed leaders. Long-term investors can take encouragement from recent equity strength, while continuing to prioritize portfolio balance through all phases of the market cycle.

Key Market and Economic Drivers in May

• The S&P 500, Nasdaq, and Dow Jones Industrial Average gained 5.1%, 8.4%, and 2.8%, respectively, for the month. All three major U.S. indices finished the month at new all-time highs.

• Volatility declined over the month, as measured by the CBOE VIX index, ending May at 15.32.

• International developed markets returned 2.6% based on the MSCI EAFE Index in U.S. dollar terms, while emerging markets returned 9.5% based on the MSCI EM Index.

• The 30-year Treasury yield reached 5.18%, its highest level in nearly two decades, before finishing the month below 5%. The 10-year Treasury yield rose to 4.4%. The Bloomberg U.S. Aggregate Bond Index returned 0.3% for the month.

• Oil prices fell with Brent crude closing at approximately $92 per barrel and WTI at $88.

• Gold ended the month slightly lower at $4,539 per ounce. The U.S. Dollar Index stood at 98.94, also down only slightly.

• First quarter real GDP was revised lower from 2.0% quarter-over-quarter to 1.6%. April inflation showed headline CPI at 3.8% year-over-year and core CPI at 2.8%.

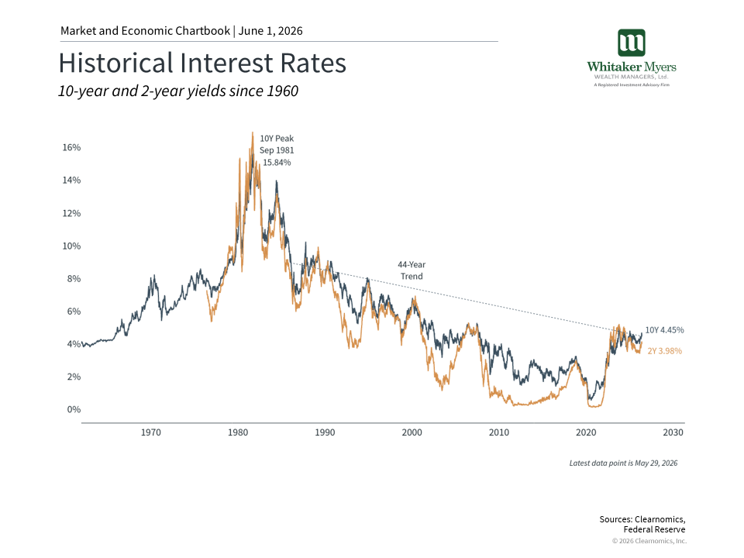

Long-term interest rates climbed sharply before pulling back

Interest rate volatility was among the most consequential developments of the month. The 30-year U.S. Treasury yield briefly touched its highest point in nearly two decades before settling back below 5%.1

Both the 10-year and 2-year yields moved higher as well, reflecting growing expectations that rates would remain elevated for an extended period. Markets now anticipate at least one rate hike by the Fed by mid-2027 in response to inflation pressures.

The Consumer Price Index and Producer Price Index both came in above expectations, driven largely by energy costs. Rising inflation tends to push yields higher, as investors seek greater compensation when purchasing power is eroding. Oil prices have declined somewhat, to around $4.30 per gallon on a national average basis, but this still represents approximately $1.50 more than before the war in Iran.2

Higher borrowing costs affect consumers through mortgages and personal loans, and weigh on businesses that rely on financing to fund operations and growth.

Despite these headwinds, perspective is important. Market expectations have shifted multiple times this year as the geopolitical situation has evolved, and interest rates have proven difficult to forecast. While rates remain elevated today, they are still well below the levels many had feared during the peak inflation period. On a positive note, higher yields now offer more meaningful income potential for bond investors, which can support diversified portfolios going forward.

Equity markets extended their run to new record levels

Despite bond market headwinds, equities continued to push higher. The S&P 500 surpassed 7,500 in May for the first time, with 22 all-time highs recorded through the end of the month.3

The Magnificent 7 and other large-cap technology names remained key contributors to market performance, though the breadth of the rally has been wider than in some prior years. Strong corporate earnings growth has supported these moves, with consensus estimates pointing to continued expansion in the year ahead.4

This constructive backdrop has also generated renewed interest in upcoming IPOs from high-profile companies such as SpaceX, Anthropic, OpenAI, and others. These companies have grown primarily through private investment, continuing a multi-decade trend of firms staying private for longer. While near-term price movements following an IPO tend to attract significant attention, the more meaningful benefit is that going public broadens the investment opportunity set for all investors over the long term.

Valuations remain a consideration even as fundamentals stay healthy. The S&P 500 price-to-earnings ratio stands at approximately 20.9x, within the range of recent years but above long-term historical averages. Elevated valuations do not reliably predict near-term market direction, but they do underscore the importance of maintaining diversification across sectors, sizes, and styles to manage risk over the full market cycle.

A new Fed Chair takes the helm amid a complex economic backdrop

Kevin Warsh was sworn in as the new Chair of the Federal Reserve in May, succeeding Jerome Powell. Warsh previously served on the Fed’s Board of Governors during the 2008 global financial crisis and brings recognized experience in monetary policy and financial markets. In his Senate testimony, he emphasized the importance of central bank independence and a focused approach to managing inflation risks.

The new Fed Chair takes office at a challenging moment. The economy remains broadly healthy, but inflation has picked up while labor market signals have been mixed. This creates a difficult policy balancing act, and markets have shifted from pricing in further rate cuts to anticipating at least one rate hike. History shows that the economy has grown across the tenures of many different Fed chairs, with earnings growth, productivity, and innovation serving as the primary long-run drivers of investment returns.

To “Sum-IT up”. May brought new milestones for the stock market, extending a strong run for investors. While headlines around inflation, the new Fed Chair, and geopolitics will likely continue to generate uncertainty, the best approach for investors is still to focus on their long-term financial goals.

References & Sources

U.S. Department of the Treasury. Interest Rate Statistics. Available at: https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

American Automobile Association (AAA). National Gas Prices. Available at: https://gasprices.aaa.com/

Clearnomics Research, based on Standard & Poor’s index data.

Clearnomics Research, based on LSEG earnings data.

CME Group. CME FedWatch Tool. Available at: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html