STAY THE COURSE: WHAT 75 YEARS OF MARKET HISTORY TELLS US ABOUT VOLATILITY, THE IRAN CONFLICT, AND YOUR WEALTH

- John-Mark Young

- Apr 5

- 7 min read

As tensions in the Middle East escalate following the Iran conflict, investors are watching the S&P 500, the international stock markets, and small and mid-sized US companies gyrate with a familiar mix of anxiety and uncertainty. Cable news has no shortage of dire predictions. Social media amplifies every down day into a potential catastrophe. Your retirement account statement might feel difficult to open right now.

Here at Whitaker-Myers Wealth Managers, we want to cut through the noise with something more powerful than opinion: data. Seventy-five years of it, stretching back to 1950 — through Korea, Vietnam, stagflation, the dot-com bubble, the 2008 financial crisis, a global pandemic, and now geopolitical conflict in the Middle East. The story that data tells is remarkably consistent, and remarkably encouraging.

"It's going to rain, so you better have an umbrella."

— Dave Ramsey

─────────────────────────────────────────

THE CONTEXT BEHIND 1950: WHY THE STARTING POINT MATTERS

─────────────────────────────────────────

Our research — consistent with our earlier article Bear Markets: Normal But Not Fun — begins in 1950, and that date is not arbitrary. Starting in 1950 forces us to include some of the most brutal periods in modern financial history.

The 1970s stagflation decade was arguably the worst macro environment of the modern era. Surging inflation, an OPEC oil embargo, a Cold War brewing, and a stock market that went essentially nowhere for a decade. The S&P 500 suffered intra-year drawdowns of -25.9% in 1970, -23.4% in 1973, -37.6% in 1974, -15.6% in 1977, and -17.1% in 1980. By any measure, a miserable environment for investors.

The dot-com bust from 2000 to 2002 saw the S&P 500 fall -9.1%, then -11.9%, then a devastating -22.1% — with intra-year drawdowns reaching -29.7% and -33.8% in those final two years. Trillions of dollars of paper wealth evaporated as the technology bubble deflated.

The 2008 Financial Crisis remains the single worst year in our entire dataset. The S&P 500 fell -37.0% on the year, with a peak intra-year drawdown of -48.8%. Banks were failing. Unemployment was soaring. The word "depression" was being used without hyperbole.

We include all of these years deliberately. It would be easy to cherry-pick a favorable starting date. We don't. And yet — across all of it — the math still works powerfully in the long-term investor's favor. The average annual return from 1950 through 2025 was +11.7%. The average intra-year drawdown was -13.6%.

Not a permanent loss. A temporary paper decline you had to sit through before the market recovered.

─────────────────────────────────────────

THE RULE OF 72: WHAT 11.7% ACTUALLY MEANS FOR YOUR FAMILY

─────────────────────────────────────────

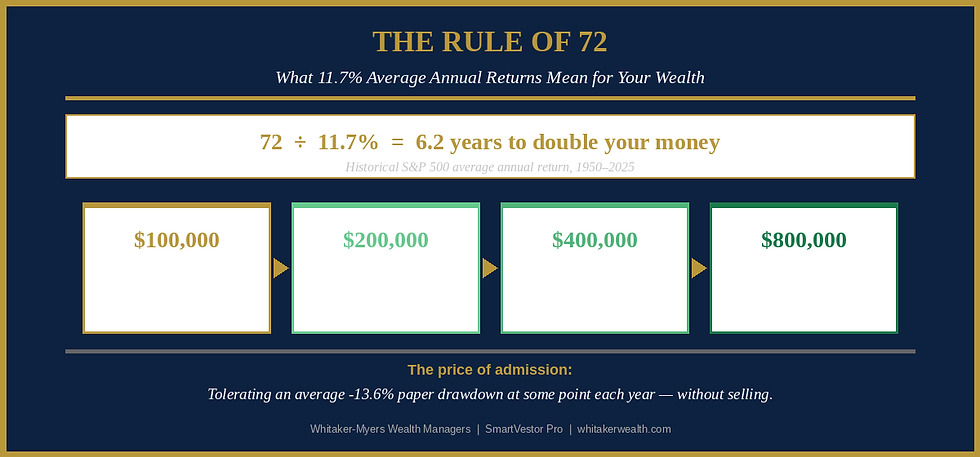

The Rule of 72 is a simple formula that Dave Ramsey references often: divide 72 by your expected annual rate of return, and you get the approximate number of years it takes to double your money.

At the historical S&P 500 average of 11.7% going back to 1950:

72 ÷ 11.7 = approximately 6.2 years to double

That means a $100,000 investment in a broadly diversified growth-stock portfolio — left alone, earning the historical average — would be expected to grow to approximately $200,000 in six years, $400,000 in twelve years, and $800,000 in eighteen years. Before you add another single dollar.

But here is the most important truth about that doubling: the price of admission is tolerating a -13.6% paper loss at some point in the average year. That is not a bug in the system. It is the feature. It is precisely because most investors cannot stomach that temporary decline — and sell — that the long-term reward exists for those who stay the course.

Dave Ramsey teaches this relentlessly: investing is not about timing the market, it is about time in the market. Every time someone panics and sells during a drawdown — whether triggered by an Iran conflict, a banking crisis, or a pandemic — they lock in a real loss and then face the nearly impossible task of knowing when to get back in. The data has never supported that strategy. Not once in 75 years.

─────────────────────────────────────────

THE S&P 500 HISTORICAL RECORD: 75 YEARS IN ONE VIEW

─────────────────────────────────────────

This table shows every year since 1950, the maximum intra-year drawdown (DD) based on closing prices, and the total return (TR) at year end. Read it slowly. Notice how many years show a red drawdown number alongside a green year-end return. The temporary pain almost always preceded a year-end gain.

A few years stand out in the context of today's environment:

1990: The Gulf War. Saddam Hussein invaded Kuwait. Oil prices spiked. Recession fears were immediate and real. The S&P 500 fell -19.9% intra-year. Frightening. And at year end? Down only -3.1%. Then it roared back +30.5% in 1991.

2020: A once-in-a-century pandemic. The market fell -33.9% from peak to trough in a matter of weeks — the fastest bear market in history. Investors who sold in March locked in those losses. Investors who stayed finished the year up +18.4%.

The Iran conflict today is creating genuine uncertainty. Oil prices, supply chains, geopolitical risk premiums, and market volatility are real. We don't minimize that. But uncertainty has been present in virtually every year of this 75-year data set. The market has not required a peaceful world to deliver strong long-term returns. It has required patient investors. Essentially, we have been in a sin-filled world the entire 75 years, and in a sin-filled world, bad stuff is going to happen.

"Time in the market beats timing the market — every single time."

— Dave Ramsey

─────────────────────────────────────────

THE DAVE RAMSEY FRAMEWORK: BABY STEPS MEET BEAR MARKETS

─────────────────────────────────────────

What should you actually do right now? The answer depends on where you are in your financial journey.

If you are on Baby Steps 1 through 3 — still paying off debt and building your emergency fund — this market volatility is genuinely not your problem today. Your wealth-building engine hasn't started yet. Keep your head down, stay on the plan, and let the market do what it does while you build your foundation.

If you are on Baby Step 4 and investing 15% of your income, keep going. Every paycheck contribution at lower market prices means you are buying more shares at a discount. Dave Ramsey calls this buying on sale. Do not pause your contributions. Do not reduce them. The worst thing you can do right now is stop investing.

If you are on Baby Steps 5 through 7, your job is to review your asset allocation with your financial advisor — not because you need to change it, but to confirm that your investment mix still aligns with your time horizon. Don't make panic-driven moves. Your long-term plan was designed for moments exactly like this one.

In every case, the answer is the same: do not sell in response to headlines. Selling turns a temporary paper loss into a permanent real one.

─────────────────────────────────────────

THE COST OF DOUBLING YOUR MONEY

─────────────────────────────────────────

At an 11.7% average annual return, your money doubles roughly every 6.2 years. A 30-year-old who invests $50,000 today could reasonably expect that to grow to $400,000 or more by retirement — before adding another dollar. That is the power of compound growth working in your favor.

But that wealth creation is not free. The cost is enduring an average intra-year decline of -13.6%. In the worst years — 1974 with a -37.6% drawdown, 2002 at -33.8%, 2008 at -48.8%, and 2020 at -33.9% — the cost is much higher. Those are the years that test every investor's conviction.

Dave Ramsey often says that building wealth is simple, but not easy. The simple part is the math: stay invested in diversified mutual funds investing in the four categories, leave it alone, and let compounding work. The not-easy part is watching your account balance decline 20% or 30% while every headline tells you the world is ending — and staying the course anyway.

The investors who built generational wealth were not smarter than the ones who sold in a panic. They were simply more patient. They understood that the drawdown was the price of admission — not a signal to leave the theater.

─────────────────────────────────────────

A WORD TO OUR CLIENTS AND COMMUNITY

─────────────────────────────────────────

Whitaker-Myers Wealth Managers exists to help families across Ohio, Florida, Georgia, Texas, and beyond build and protect wealth using time-tested, biblically-grounded financial principles. We are Dave Ramsey SmartVestor Pros because we believe in the Baby Steps: get out of debt, build a fully-funded emergency fund, and then invest consistently for the long term.

Markets will always have scary years. Iran today. Something else tomorrow. The data does not promise a smooth ride. It has promised a rewarding destination for those who stay in the vehicle, and the most likely future outcome is the same. We don't know by how much, how quickly and if it'll be as good, but that's ok.

Matthew 6:25-34 (ESV) reminds us to not worry about how much the stock market will grow today, tomorrow or the future. 25 “Therefore I tell you, do not be anxious about your life, what you will eat or what you will drink, nor about your body, what you will put on. Is not life more than food, and the body more than clothing? 26 Look at the birds of the air: they neither sow nor reap nor gather into barns, and yet your heavenly Father feeds them. Are you not of more value than they? 27 And which of you by being anxious can add a single hour to his span of life?[a] 28 And why are you anxious about clothing? Consider the lilies of the field, how they grow: they neither toil nor spin, 29 yet I tell you, even Solomon in all his glory was not arrayed like one of these. 30 But if God so clothes the grass of the field, which today is alive and tomorrow is thrown into the oven, will he not much more clothe you, O you of little faith? 31 Therefore do not be anxious, saying, ‘What shall we eat?’ or ‘What shall we drink?’ or ‘What shall we wear?’ 32 For the Gentiles seek after all these things, and your heavenly Father knows that you need them all. 33 But seek first the kingdom of God and his righteousness, and all these things will be added to you.

34 “Therefore do not be anxious about tomorrow, for tomorrow will be anxious for itself. Sufficient for the day is its own trouble.

If you have questions about your specific situation, your asset allocation, or whether your plan is positioned correctly for this environment, please reach out to one of our advisors. We are here for you.

The rain Dave Ramsey warned you about has come for a bit this year, and soon it will be a bright sunny day. Make sure you have your umbrella — and don't let the storm push you out of the market.