Hopefully, you'll excuse my two-week hiatus from "What We Learned in the Markets." I'll be back next week and better than ever when I bring the four things I learned in the market while spending time with my family. But to whet your appetite, let's talk about what the last two weeks' strong inflation data and employment info have meant to the Fed's soft landing hopes.

Ten dollar words to describe two-dollar concepts. That's how I feel about the term soft landing. If you listen to business news or even office chatter, you have heard the term soft landing, thrown around and shaken your head like you fully understood the term and concept. Essentially, it's this: a controlled landing of a plane, spacecraft, or other flying object without serious damage. That it's my friends, minus the airplane. The Fed is trying to slow down the economy to kill inflation without doing serious damage to the economy. The same can not be said about the markets. You can tell by your 2022 401(k), IRA, or other investment statements. However, the Fed is concerned about the totality of the economy.

Market and economic expectations have shifted 180 degrees since the start of the year when many investors expected a recession and prolonged bear market. Ongoing economic growth, low unemployment, improving price pressures, and slowing Fed rate hikes have spurred a strong market rally, especially across sectors that struggled last year. While the economic situation is far from perfect and investors should always be prepared for uncertainty, it's also important to recognize the positive trends that are raising the odds of a "soft landing." What factors are driving these changes in investor expectations?

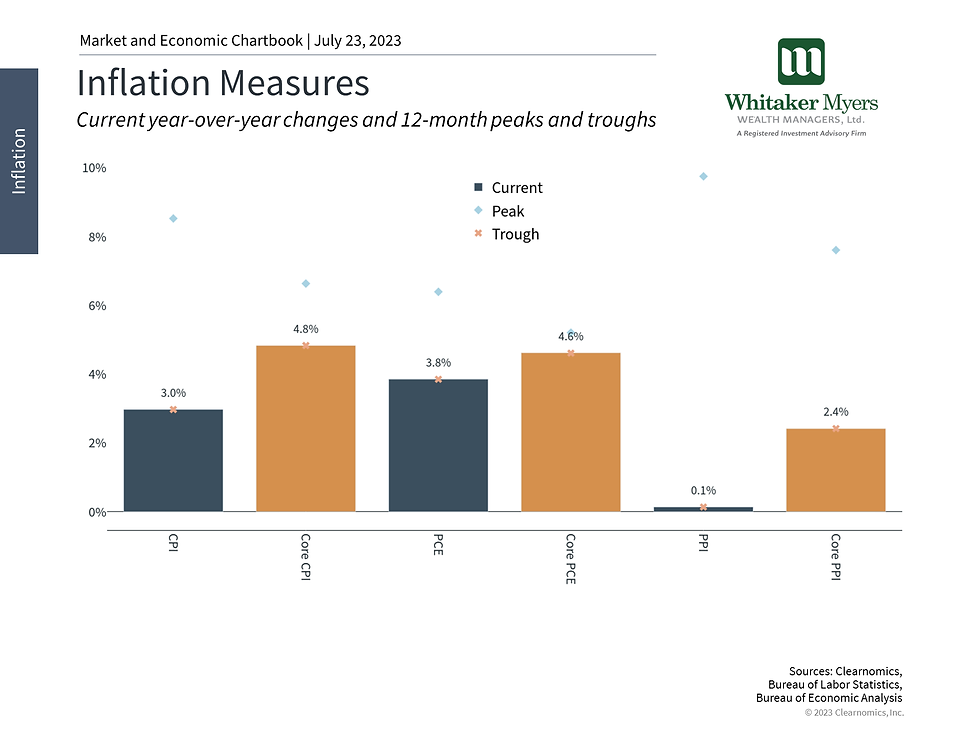

Inflation is improving across many measures

Perhaps the most important are the many signs that inflation is improving. Recent data for both consumer and producer prices show meaningful signs of deceleration toward Fed targets. The Consumer Price Index (CPI) has slowed from a peak year-over-year rate of 9.1% a year ago to only 3% today. Similarly, the monthly rate of 0.2% for headline inflation represents an annualized rate of 2.2% - very close to the Fed's 2% target. Core inflation remains elevated at 4.8% when comparing prices this year to last year. However, the monthly pace slowed in June to only a 1.9% annualized pace. These are all positive signs and suggest that while prices could remain high, there is already far less upward pressure.

Producer prices show even greater improvements. Headline Producer Price Index figures (for "final demand") show a year-over-year change of only 0.1% in June. Core PPI rose 2.4% compared to last year, but only grew 0.1% month-over-month. Other measures showed sharper improvements and even deflationary trends, especially among "intermediate demand" which represents industries buying the inputs they need. These data suggest that prices are declining throughout the supply chain, creating additional hope that these gains will eventually be passed on to consumers.

Of course, there are always caveats. On a technical basis, the year-over-year comparisons will likely worsen next month. This is because the peak rate of inflation occurred exactly a year ago so future comparisons will become more difficult. This means that, going forward, it will be more important to focus on the current pace of inflation rather than how prices compare to last year. Additionally, many of the headline improvements have been in volatile areas like energy, which can always fluctuate. Finally, shelter prices (rent and "owners' equivalent rent") declined in June but the pace of improvement has been quite slow so far, and it's difficult to know whether this will be sustained.

The Fed expects to raise rates again after pausing

For the Fed, which has been grappling with the largest inflation shock since the 1970s and early 1980s, these data could not have come at a better time. The Fed decided to skip a rate hike in June in order to "allow them more time to assess the economy's progress toward the Committee's goals of maximum employment and price stability," according to the latest FOMC meeting minutes. In other words, the Fed had already decided to slow the pace of rate hikes from 25 basis points every meeting to perhaps every other meeting.

The accompanying chart shows that Fed officials expected to raise rates two more times later this year (i.e., an additional 0.5%). At the moment, markets are anticipating only one additional hike. This disconnect between the Fed and markets has driven volatility over the past year, with the Fed staying firm and markets adjusting to meet monetary policy. In general, a slower pace of rate hikes, if justified by the economic data, has been cheered by markets as this year's S&P 500 return of 17% shows.

Wage growth is still strong despite improving inflation?

The Fed's challenge since they began raising rates in March 2022 has been to strike a balance between beating inflation and preventing a recession, i.e., achieving a so-called "soft landing." The absence of a recession so far, alongside these inflation data, is positive and a big reason for this year's market rally. Current consensus forecasts by economists still call for flat GDP growth in the third quarter and slightly negative growth in the fourth before rebounding next year. Over the past twelve months, these forecasts have been revised upward with recession forecasts continually pushed back.

What has helped is the strength of the labor market. The latest report from the Bureau of Labor Statistics shows that 209,000 net new jobs were added in June, a slower but still very healthy number. Unemployment continues to hover around 3.6%, near historic lows. Wage growth is strong with average hourly earnings rising 4.7% on a year-over-year basis. Despite earlier layoffs in tech, there are still 9.8 million job openings, or about 1.6 openings per unemployed person, which suggests that many businesses would like to hire if only they could find qualified workers.

Theoretically, higher wages should make inflation stickier as consumers spend more and the cost of doing business rises. Thus, higher wages in a disinflationary environment are somewhat surprising given that economic theory typically assumes that there is a tradeoff between inflation and jobs. Additionally, perhaps an even bigger fear investors faced last year was around the possibility of stagflation - a period of poor growth in which inflation remains stubbornly high. While it's too early to declare victory, updated expectations by investors and economists suggest that these scenarios are now less likely.

The bottom line? The current economic environment is far from perfect but is still significantly better than what many had feared only six months ago. This is a reminder that consensus views are not always correct and can change rapidly as conditions shift. That said, with markets having priced in a return to normalcy already, it will be important to stay balanced as the inflation, Fed, and economic situations evolve.

WHAT THE HOPE OF A SOFT LANDING MEANS FOR THE FED AND INVESTORS

July 23, 2023

John-Mark Young

Whitaker-Myers Wealth Managers is an SEC-registered investment adviser firm. The information presented is for educational purposes only and intended for a broad audience. The information does not intend to make an offer or solicitation to sell or purchase any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. Whitaker-Myers Wealth Managers reasonably believes that this marketing does not include any false or misleading statements or omissions of facts regarding services, investment, or client experience. Whitaker-Myers Wealth Managers has a reasonable belief that the content will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Please refer to the firm’s ADV Part 2A for material risks disclosures.

Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances of market events, the nature and timing of the investments, and relevant constraints of the investment. Whitaker-Myers Wealth Managers has presented information in a fair and balanced manner.

Whitaker-Myers Wealth Managers is not giving tax, legal or accounting advice, consult a professional tax or legal representative if needed.

Copyright (c) 2023 Clearnomics, Inc. and Whitaker-Myers Wealth Managers, LTD. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.